CREDIT REPAIR post bankruptcy

So you have filed. If you decided to keep paying your car payment under good terms, you are already on your way to re-establishing. What else should you do? More important - should you not do.

You have your discharge papers in hand. The fresh start begins, but everyone says no for new credit or the interest rate is crazy high. Does not seem like a fresh start? Where to begin? I WROTE THIS BACK IN 2011 WITH A FEW EDITS! NOW I HAVE BE FINANCIALLY FIT!

It is highly recommended that you attend a seminar for obtaining a home loan in your area! The tips are incredible and will have you on the right track.

The tips here are limited, general and not legal advice. They are from experience and my seminars. There are much more in-depth classes and ideas.

If your goal is a home, please start working with your experienced loan officer two years in advance. Pick the bank you would like to work with and attend all their home buyer classes!

SEVEN YEARS LATER I AM OFFERING THESE HOME BUYING CLASSES... It is exciting to come back after all these years and note the progress in the services provided.

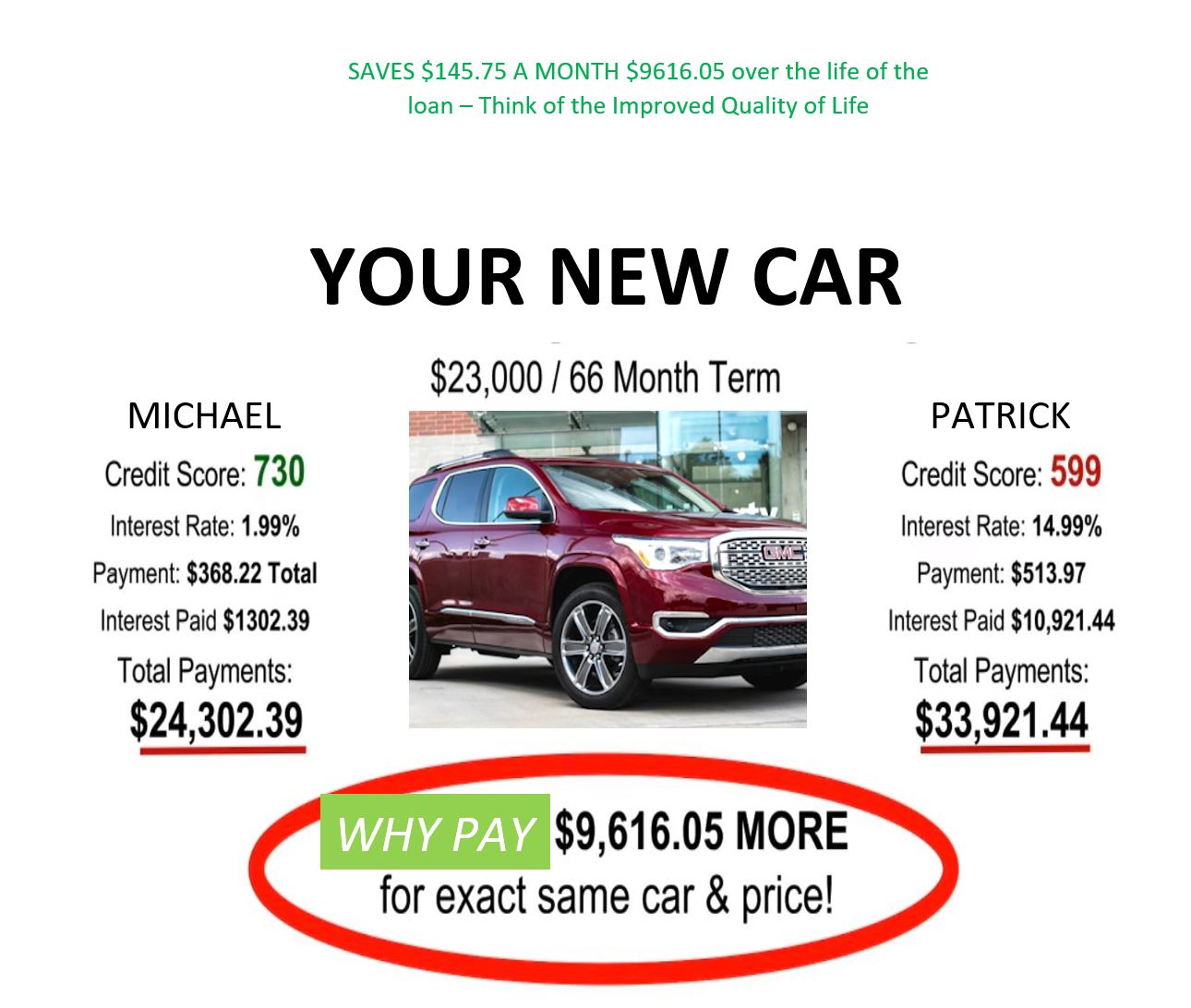

Take the time to compare the interest on 29% interest car loan with a 0% interest car loan over 60 months on a $25,000 car. check out these numbers:

car interest payment life of loan

$25,000 1% $427.37 $25642.20

$25,000 29% $793.55 $47613.00

The loan owner with bad credit pays nearly double for the same car!

So, it saves a great deal of money to rebuild the credit through other means than a car loan if the interest rate is crazy!

Monthly expenses are dramatically lower and overall quality of life will be significantly improved by patiently rebuilding with another means besides a vehicle.

This is one reason why people decide to keep their car during the bankruptcy.

CONSIDER what benefit could a client receive from having their attorney look at your circumstances and recommends reaffirming the terms of their car loan. Often reasonable (10%) interest rate about the value of the car! Sometimes this is much better to keep the current car at market value than surrendering a reliable car and purchasing another high interest car later that will be off the lot - NOT market value.

An Example: Here is how I did it for my daughter. She turned 18 March 2012. I will not under any circumstances co-sign a loan for my children unless I intend to pay it in full. So, the two lines of credit she started with are:

1) Furniture credit line approved $1000 with a zero interest if paid in time loan. She purchased a video camera. She paid about $200 more for this item since they were offering the line of credit. You wont get the great interest rates until you proof yourself. If family and friends wont back you -- why should a bank?

2) Bronco Federal Credit shared loan - She put $500 put in a secured savings account. They loaned her back her own $500. She could spend the cash and pay it back in small monthly payments at 2% (yes 2%) interest, or she can put it in a savings account and have the bank make the payments on time for her! This line of credit runs about the same cost as a super sized meal at a fast food joint over the life of the loan.. and looks fabulous.

3) We added her to one of our lines of credit as an authorized user.

When she is ready, if she ever wants to purchase a new vehicle, she will not have the enormous interest rates most people pay. They have 2% - 3% deals she can strive for.

UPDATE 2018 = She decided not to finance a car... Her and her husband bought a house in 2017 at a great interest rate. Why? They did not overextend. They did not miss payments or bounce checks or leave medical debts unpaid. They earned credibility. They were now trustworthy. When you first met a friend, would you loan them money?

Granted this process is much easier for the employed (wage earners), it does still work for self-employed.

The biggest error is applying everywhere and thinking someone will say yes. It hurts your credit score every time you inquire after the reasonable amount (which is only a few in a six months period).

The second error is getting a car at enormous interest right off the lot! You could try a private purchase car loan (newer cars, just not new) at a regular bank or credit union if you have some equity or other ideas -- you can call BFF now to discuss.

You can even build credit with the car you currently have title to in some cases.

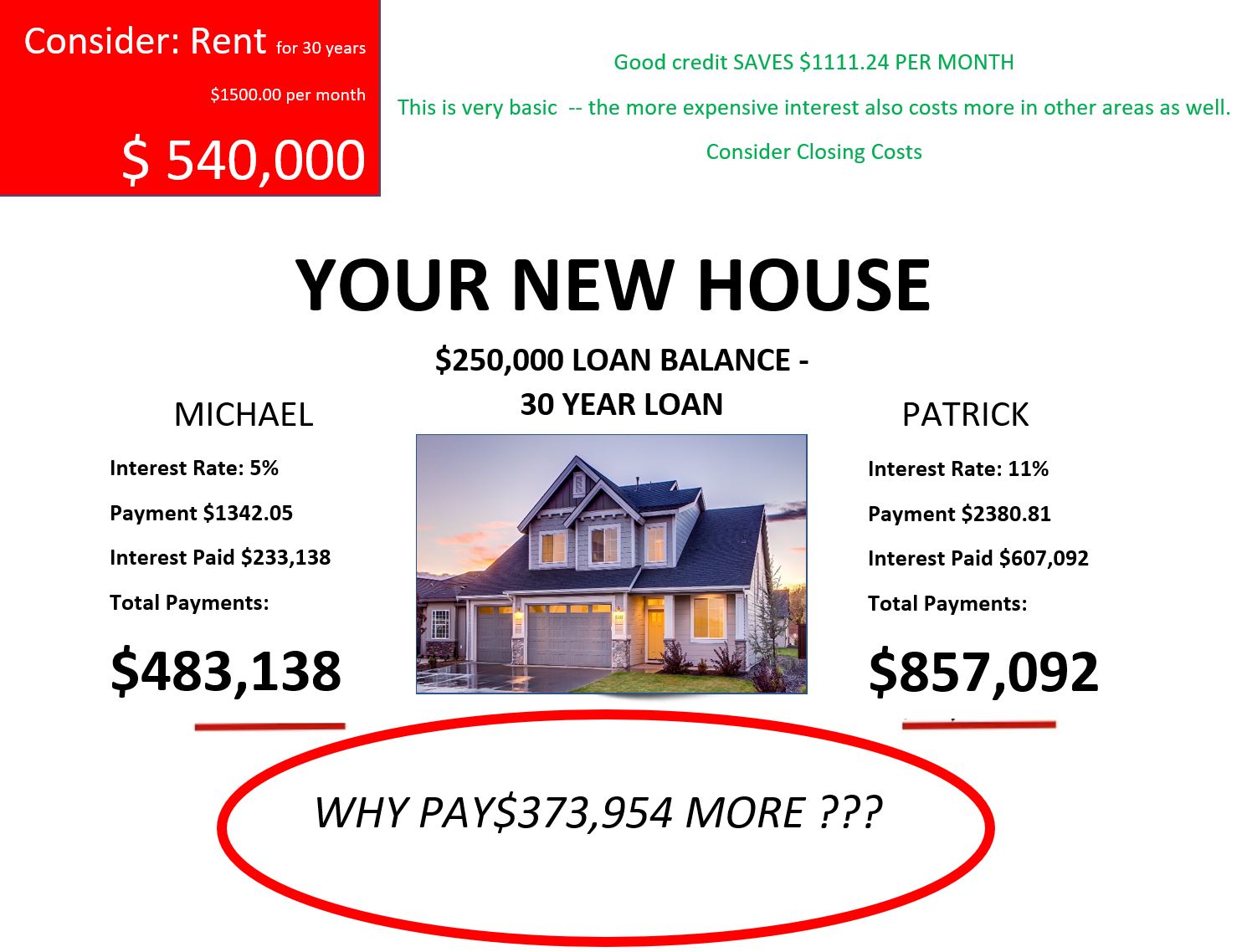

In the above situation you can see a car can cost you a few thousand financing the wrong way, a house can cost into the hundred(s) of thousands with the wrong financing.

RECENT EXAMPLE: I was just told a FHA through Quicken had closing costs of about $5500 and an interest rate of 4.99 (this is June 8. 2018) where the conventional loan is thousands less with a 4.50 interest rate. The sole difference - credit cards are charged at 75-90 percent. The decision was to wait to refinance until the cards are paid down to 69% or below. This refinance would cost almost an additional $190000 over the life of the loan to consolidate $48000 in debt. The lender said it would "only increase the monthly payment to less than $400 a month." YET... it also adds $53000 to the loan if the house needs sold. It also adds the three years to the current 27 year loan!

Look below at an actual home loan example. You can buy another house right out of bankruptcy or even foreclosure if you have the down payment.

Of course, someone - if they keep their credit good, and if they keep their debt to income good, and if their job stays stable - they are going to refinance the higher interest home. If.

Now consider that cost too! There are expensive closing costs to buy and closing costs to refinance. But is it more expensive than giving rent money to a landlord every month? Every case is different.

Before or After your Bankruptcy - Call us at Be Financially Fit - it is a free consultation. Free education - many financial situations you can handle yourself. However, sometimes you will need to speak to an expert and/or someone that can provide legal advice. You will be referred to credit attorneys or bankruptcy specialists or a loan specialist as needed or wanted.

BROKER INFORMATION

Rica Jo Ann Gilmore, Broker, Realtor®

- Graduate, REALTOR® Institute

- Accredited Buyer's Agent

- Seller Representative Specialist

- REALTORS® Commitment to Excellence

- Military Relocation Professional

- Seniors Real Estate Specialist®

- Short Sales and Foreclosure Resource

- Pricing Strategy Advisor

- Home Measurement Specialist

- Real Estate Negotiation Expert

- Certified Team Specialist

|

Current Affiliates SeanCo 2019-present, Rica Realty @ 2023, Rica Realty LLC @2023

Previous Affiliates HCLA, LLC 2018-2023 Process My Papers @ 2006-2018

All rights reserved.

The listings data displayed on this medium comes in part from the Real Estate Information Network, MLS (REIN) and has been authorized by participating listing Broker Members of REIN for display. REIN listings are based upon Data submitted by its Broker Members, and REIN Therefore makes no representation or warranty regarding the accuracy of the Data. All users of REIN MLS database should confirm the accuracy of the listing information directly with the listing agent.

REIN and/or Rica J. Gilmore and information is protected under federal copyright laws. Federal law prohibits, among other acts, the unauthorized copying or alteration of, or preparation of derivative works from, all or any part of copyrighted materials, including certain complications of Data and information. COPYRIGHT VIOLATORS MAY BE SUBJECT TO SEVERE FINES AND PENALTIES UNDER FEDERAL LAW.

Information Deemed Reliable But Not Guaranteed

This website contains information related to law and is NOT LEGAL advice. It contents is for information only. If you need legal advice, please consult an attorney or act as your own.